Africa’s evolving energy landscape | S&P Global Commodity Insights

Oil and its byproducts have been gathered in Africa for thousands of years. Egyptians used it as glue, a component for waterproofing as well as for embalming. There is even reference to bitumen being used in the coating of Moses’ basket.

That said, it wasn’t until the mid-1950s that oil exploration really progressed in north Africa, with the first giant and super giant discoveries, and when the Nigerian joint venture between Shell and BP started to bear fruit.

Algerian super giants Hassi Messaoud and Hassi R’Mel were discovered in 1956 and 1957, followed by the Libyan Sarir group of fields in 1961. In West Africa, more than 20 fields holding in excess of a billion barrels were discovered between 1958 and 2000.

After seeing staggering success, oil and gas companies doubled down in established regions, sending liquids production to an all-time high of just under 10 million b/d between 2006 and 2008, according to S&P Global Commodity Insights.

Download the latest Commodity Insights Magazine. Features include:

* The future of energy

* Carbon market challenges

* * Europe’s race to energy security

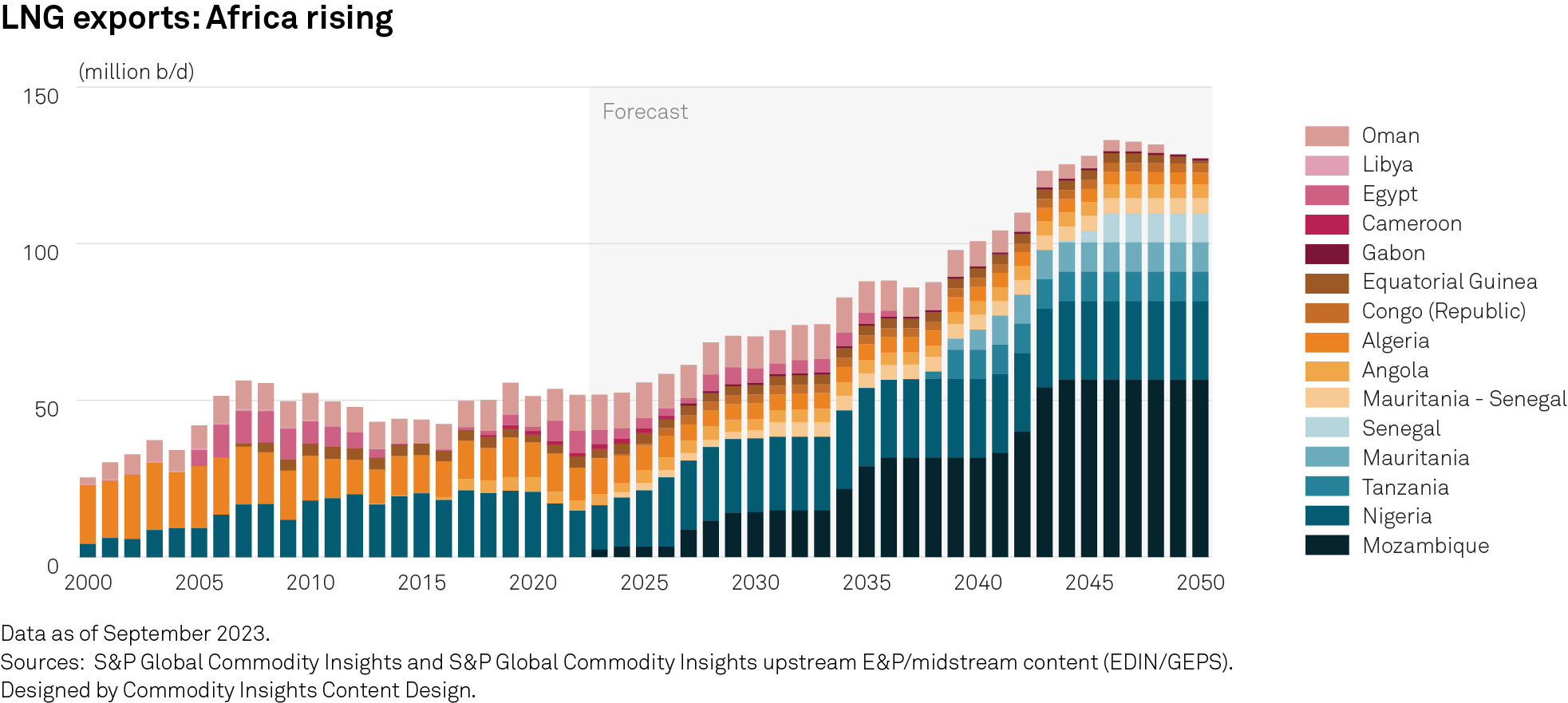

In 2006, exploration focus started to shift to new frontiers and the discovery of 170 Tcf of gas resources between 2010 and 2015 offshore Mozambique and Tanzania set the continent on a new path.

This change in trajectory is now tying into the larger global energy transition where gas forms a cornerstone and where Africa’s hydrocarbons play a far larger role in powering the continent.

Shifting European energy security demands as a consequence of the Russia-Ukraine war mean that further developing Africa’s vast gas resources has climbed the strategic agenda for consumer governments and upstream companies, creating new economic opportunities for host countries.

LNG developments in Mozambique could ultimately result in the country becoming Africa’s largest exporter of LNG. The BP-operated GTA development offshore Senegal and Mauritania, and Eni-operated Marine XII development in the Republic of Congo will both start production in 2024, while new gas export projects could be sanctioned in Nigeria and Tanzania, along with additional developments in Mozambique and Senegal.

In just two years Africa has or will add three LNG exporting countries to its portfolio. As we look toward the end of the decade, gas developments offshore Namibia and South Africa will play an important role in power security.

Dwindling role of coal

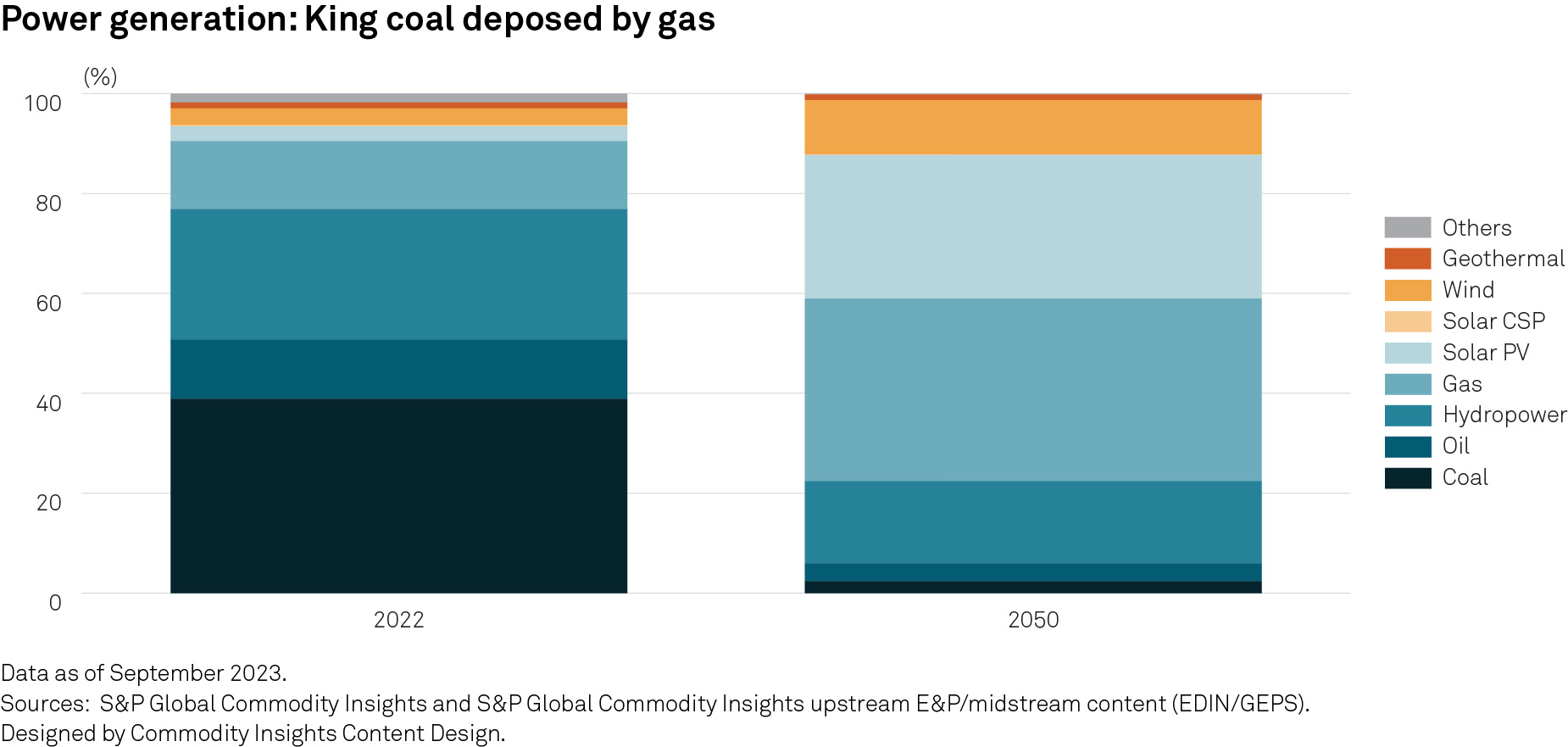

In Sub-Saharan Africa coal-fired power plants currently account for almost 40% of electricity generation capacity. However, many of these plants are aging and finding financers that are willing to finance new coal power projects is becoming increasingly difficult.

The exit of China from new developments due to a change in its global strategy – with a greater focus on clean energy – will be particularly impactful, leaving the existing project pipeline with little or no prospects for international investment.

As coal-fired power generation is retired it will be replaced by renewable and gas-fired power.

By 2050, gas could account for some 35% of power generation on the continent, with coal accounting for less than 3% according to S&P Global Gas Power and Renewables Research.

Growing significance of gas

Africa is poised to play an important role in a world that is moving toward increased gas consumption. Africa’s liquefaction capacity currently stands at nearly 75 million mt/year. This should increase to just under 130 million mt/year in early 2040, according to S&P Global LNG research, and include several new LNG exporting countries. This has been made possible by companies pushing into new frontiers and establishing regions set to become gas mega hubs.

As Africa increasingly understands the role it will play in powering the world, countries are vying for capital across both the oil and gas sector and the clean energy space. This competition is taking place on several fronts – from fiscal attractiveness to the perception of stability. Countries viewed as stable, such as Namibia, Morocco and Egypt, are outcompeting those perceived to be riskier. Countries with more conducive fiscal terms are attracting more exploration capital. As a result, mature producers such as Angola are actively improving terms to compete with more frontier regions to entice exploration. Africa’s energy landscape is evolving, and this development – along with the continent’s approach to the energy transition – could ultimately have an important impact on the world’s energy balance.

With James Taverner, Silvia Macri and Laura Sima

This article first appeared in the February 2024 edition of the

Commodity Insights magazine

.