Commodities Get Pulled Into the Global Short-Volatility Trade

(Bloomberg) — Traders are betting against volatility in raw materials prices, countering the commodity sector’s notoriously boom-and-bust history.

Most Read from Bloomberg

Whether it’s an oil market that is stuck firmly in a range due to OPEC+ cuts and abundant spare capacity, or copper prices torn between surging renewable demand and strains in more traditional consumption areas, there have been plenty of factors keeping the world’s commodity prices stuck in recent months. Gas volatility is back to where it was before a supply crisis in Europe.

It makes for another sector in global markets where one of the most dominant trades has been betting against big swings. Macro volatility has been grinding lower as equities push higher and billions of dollars pour into exchange traded funds wagering on continued calm.

It’s unusual to see such a prolonged period of stagnation in commodities, though. From the Covid-19 pandemic to Russia’s invasion of Ukraine, there have been a steady stream of events in recent years that have led to wild swings in prices and bumper profits for the world’s biggest traders of those raw materials.

“It’s clear that we’re not in a momentum year for commodities at least,” said Jo Harmendjian, portfolio manager at Tiberius Group AG. “The only thing that can make you money is to find structures that can make money if nothing happens, a carry trade generated by selling vol wisely.”

Betting on subdued prices is all the more risky in a highly volatile world, as Russia continues its invasion, Yemen’s Houthi rebels attack ships in the Red Sea and swaths of the global economy go to the polls this year. A sharp rally in the copper market on Wednesday offered a reminder of the risks involved for those betting on ongoing inertia in markets where supply risks still loom large.

Betting against market volatility generally entails selling options contracts that won’t expire with value. It’s a process that is much the same as being an insurance provider — a trader keeps the premium a counterparty pays them if the contract doesn’t pay out, but if it does then they risk big losses.

Some metals like zinc and aluminum have suffered after spiking on supply losses arising from the energy crisis. Now they’ve been hammered by a sharp downturn in industrial demand. Implied volatility for zinc is at a three-year low, while aluminum is close to a four-year low. Natural gas volatility has tumbled in Europe as prices retreat thanks to a mild winter and healthy stockpiles too.

Grinding range-bound trading in metals markets has proven painful for some hedge funds who were using options to bet on big rallies last year, and the rising popularity of short-volatility trades reflects a shift in tactics as investors look to eke out returns in listless markets.

Risky Business

But build ups in short volatility positions come with risks, as they can potentially exacerbate the next move in commodity markets when traders scramble to unravel those positions.

A major slump in commodities volatility that was followed by a spike in 2018 saw one relatively small fund liquidate in the face of losses that could have exceeded $150 million.

There are some notable exceptions to the becalmed markets. Gold volatility has been climbing as prices power to record highs and cocoa markets are facing major scarcity, also creating big price swings.

But elsewhere, commodities are mirroring the trends seen across global markets.

Volatility in European natural gas options has fallen to levels last seen in December 2021 — months before Russia’s invasion of Ukraine sparked a market crisis. Sluggish economic growth has also played a part, sapping energy demand in major industrial hotspots such as Germany.

Still, the region remains vulnerable to unexpected supply disruptions after losing most of its Russian pipeline fuel imports.

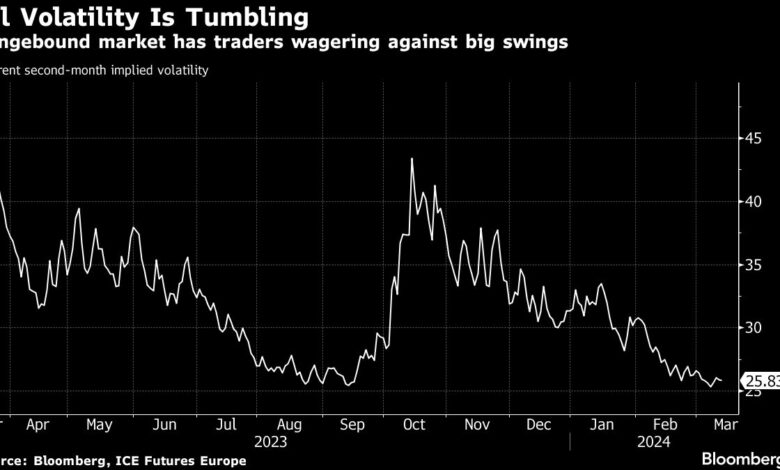

In the oil market, the signs of stagnation are clear. Brent crude futures have just endured their narrowest weekly price range in two-and-a-half years. Volatility there recently fell to the lowest level since January 2020, with traders at a recent London oil gathering lacking strong conviction about an imminent big move in either direction.

“Low macro volatility is definitely contributing to lower implied volatility in oil, but the fact that prices have been rangebound over the past few weeks is likely the strongest reason for it,” said Anurag Maheshwari, head of oil options at Optiver. “Systematic volatility selling strategies have also dominated the flow.”

–With assistance from Anna Shiryaevskaya.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.