Australians choke on mortgage debt

The Reserve Bank of Australia (RBA) released data on Australia’s debt servicing to June 2023, which captures the first 4.0% of official cash rate hikes but excludes the most recent 0.25% increase on Melbourne Cup Day.

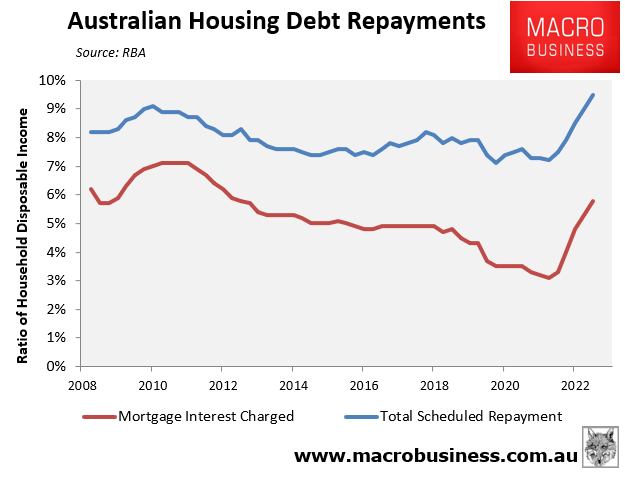

As shown in the next chart, the share of aggregate household income devoted to paying mortgage interest rose from a low of 3.1% in March 2022 (before the first rate hike) to 5.8% as of June 2023.

Overall scheduled mortgage repayments (comprising both interest and principal) rose from 7.2% in March 2022 to a record high 9.5% of aggregate household income as of June 2023:

Advertisement

Combining the RBA’s figures above with the Bank for International Settlements (BIS) debt servicing ratio (i.e. principal and interest repayments as a share of household income) delivers the following chart:

As you can see, the BIS has recorded a far bigger share of Australian household income going towards principal and interest debt repayments, which likely reflects differences in data methodology between it and the RBA.

Advertisement

Regardless, the above chart shows that Australians were sacrificing a near record share of their incomes toward servicing their debts in June 2023.

Australians have also been hit with higher mortgage rate increases than most peer nations, reflecting Australia’s unusually high share of variable rate mortgages:

Advertisement

Moreover, given the RBA lifted the official cash rate again in November and large volumes of mortgages have since transitioned from ultra cheap pandemic fixed rates to variable, it is highly likely that Australian households are now spending a record share of their incomes repaying debts.

The good news is that the RBA seems unlikely to hike rates again and could even begin an easing cycle in the second half of the year.

The bad news is that Australia’s unemployment rate is likely to rise sharply in 2024, which will increase the vulnerability of highly leveraged households.

Advertisement