FXI: China 2024 – The Year Of The Paper Dragon (NYSEARCA:FXI)

GOCMEN

In my view, the Chinese stock market is one of the most important financial news stories for 2024. In recent months, China has experienced another crash in its precarious stock market as its economy enters a debt-deflation spiral. Surprisingly, this fundamental change has received little attention in most US financial news media, potentially because China’s economic tides are believed to have little impact on the US market. However, if we consider the currency market interventions that may occur in China, we can see how bearish events in China may lead to a rebound in some inflation and interest rate issues in the US.

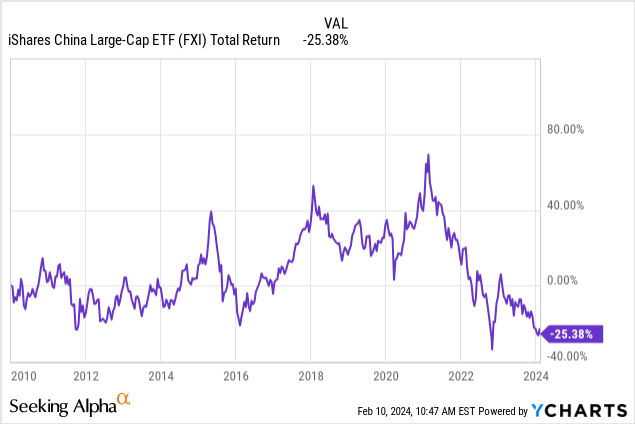

In 2022, I covered the iShares China Large-Cap ETF (NYSEARCA:FXI) in “FXI: Chinese Stocks Are Down 50% Over The Past Year And May Continue To Slide.” Since then, FXI has lost an additional 26% of its value. Most analysts have consistently been bullish on FXI due to its low valuation but may be overlooking China’s severe economic issues and poor equity market regulation. Thus, the problems facing FXI are multifaceted. Further, I believe that if FXI breaks below its current support level, a series of events may occur in the FX market that will have severe consequences for the US monetary system and, therefore, the US stock market. As such, investors should pay attention to FXI in the following weeks and months as it may be a harbinger of coming events in the US market.

Why China’s Economy is a Paper Dragon

The idea that China’s economy is a “paper dragon” has existed for some years. If we look back to the 2000s and early 2010s, China was often seen positively due to its tremendous economic growth rate and shift toward Westernization. However, as its economic growth has slowed, China has arguably shifted back toward an isolationist focus. Further, much of China’s economic growth has not translated into a transition toward a resilient service-centric economy.

Indeed, much of it is based on debatable data. Years ago, the Federal Reserve did a study that estimated that the economy’s GDP was overstated by a staggering 65% based on satellite data. These overstated economic data figures have arguably worsened since then as its economy has slowed. Further, China boasts the most expensive homes in the world from a price-to-income perspective (among larger countries); however, around a quarter of these properties are vacant, used as “investments” for household wealth (~70% of wealth in real estate). China also has terrible population demographics, with far fewer < 30-year-olds than > 30-year-olds, meaning the vacancy rate is guaranteed to worsen (without immense migration or massive property demolition).

Much of China’s economy is based on building properties and infrastructure that will never be used and supplying financing for this practice. Thus, four out of five of the largest banks in the world are in China. Even using official numbers, which are likely overstated, China’s total debt-to-GDP and private debt-to-GDP are worse than the US, which has notoriously high debt.

A third of FXI’s assets are in financials and real estate, directly exposing them to this crisis. However, as seen in their terrible recent performance, even the less exposed holdings like Alibaba (BABA) and Tencent (OTCPK:TCEHY) have proven to be at risk. Fundamentally, as Chinese people struggle more with the property market and debt bills, they’re spending less on the already minimal consumer spending they have. Because the CCP intervenes so much, virtually all of China’s sectors rise and fall together because the CCP essentially redistributes profits across the economy, for example, by increasing taxes on technology while trying to stimulate its other industries.

The Bubble is Popping Despite CCP Efforts

Overall, even if we assume China’s financial and economic statistics are accurate, its economic position is far worse than that of the US, with its only positive factor being its massive net exports. This bubble has grown over the past two decades, and many believe its government can stop it from popping, but recent trends suggest that it cannot kick the can down the road any longer. For one, consider China’s primary economic battle against falling home prices. Should home prices fall, many Chinese people will be underwater due to the immense spending on this sector. As shown below, home prices are now falling despite consecutive cuts to the cash reserve ratio:

China Home Prices vs. Cash Reserve Ratio (TradingEconomics.com)

Historically, China has managed to keep home prices from falling by cutting banks’ reserve requirements and encouraging more lending. However, today, this is not sufficient to increase its economy. Most of its GDP data points to a slowdown, but it is hardly reliable due to solid evidence of consistent manipulation. Still, it is in a deflationary spiral, even with bond yields falling below 2.5%. See below:

China 10 Year Yield vs. Inflation (TradingEconomics.com)

While most Americans do not like high inflation, deflation is arguably much worse, mainly when private debt levels are so high. Prices for goods and homes are falling in China, but because most bought these homes (often buying second homes as investments) at higher prices, they’re now underwater. Since inflation is so low, labor costs are now falling in China, while weekly hours are rising, currently at 49 hours per week (compared to 34 in the US and 31 in the UK).

Thus, Chinese workers are now working harder for less pay to try to keep up with the deflationary debt spiral. More time at work equals less time buying discretionary items. Hence, China’s consumer confidence has collapsed to an all-time low, but its consumer debt is still rising, indicating the debt-deflation spiral is accelerating. Nearly a third of FXI’s holdings are in consumer discretionary stocks directly exposed to this significant issue.

FXI Outlook For 2024

I believe the Chinese economy and financial system have passed the point of no return. At that point, the CCP can, at best, slow the inevitable collapse of the bubble it has enabled over the past twenty years. Again, I say this is a certainty, considering so much household wealth in China is wrapped up in properties with no fundamental value, such that nobody will ever live in most of its ghost cities (considering its negative population trend). In my view, the immense debt carried by households and developers due to this effort is so vast it makes the US appear highly solvent.

The CCP has not delayed the issue despite consecutive reserve requirement cuts and other efforts. As more banks see higher bad loans, its stock market, which has never returned a dime during the past ~17 years, is now being propped up by the CCP. Still, it will remain at its support level from the end of 2022. See below:

Some believe FXI will rebound due to the CCP’s recent decision to buy stocks outright to stop the crash. That may be enough reason not to short-sell FXI, as it is rarely wise to bet directly against those who can print money. However, I firmly believe any rebound will be yet another dead-cat-bounce.

Investors have considered FXI’s low valuation and China’s high “GDP” growth rate positive points; however, FXI has never delivered lasting returns since ~2006. iShares marks its “P/E” at 10.3X, but excludes stocks with negative “P/E” ratios, making it a not useful figure.

Further, FXI owns H-Shares, not A-Shares, which are only available to Chinese buyers. Put simply, this means that foreign investors in China are treated at a lower protection tier. For example, with the Evergrande (OTCPK:EGRNQ) bankruptcy, domestic investors will receive some payout while foreign investors likely will not. Country Garden (OTCPK:CTRYF), an even larger developer, defaulted on its overseas debt last year but not its domestic debt.

In my view, if we consider the high probability of an extensive and prolonged financial market crisis in China, its historically poor stock market return, and its total lack of respect for foreign investors, FXI is indeed an uninvestable asset today. Quite frankly, investors would be unwise to trust all of the data from these firms, considering so much economic and accounting data in China is misrepresented or false, while those who try to publish the data are often penalized or worse. According to US regulators, the audits of Chinese companies are highly deficient. Even worse, if they fail, and I expect many will, foreign investors will be the first to lose all their investments.

Put simply, I believe FXI is an investment in a broken communist system, and communism rarely pays foreign capitalists well. I am very bearish on FXI and think it will continue to lose value as its debt deflation spiral accelerates. That said, I would not short FXI or other Chinese assets because they could rise temporarily as the CCP pulls out all its stimulus tools to delay or slow the crisis.

Carryover to the US Economy?

On the one hand, while foreign investors give a lot to China, despite its poor equity market performance, Chinese investors do not own significant US equity assets. There is a low degree of direct exposure of the US market to China. However, if we account for the currency and bond market, there is a high probability of carryover.

The US is such a significant importer from China that it cannot avoid this exposure. For now, Chinese workers are working more hours for lower pay, indirectly keeping import prices from rising. However, the social unrest following the financial crisis may easily upset that situation. As is often the case, China’s ever-growing hawkish tone regarding Taiwan may be an effort to distract its population from its growing domestic instability.

China owns a considerable amount of US debt, likely around $6T in total reserves. China has reallocated its reserves but has not sold US debt to prop up its currency or market. Indeed, the Chinese Yuan is about the weakest it has been in over 16 years due to its growing economic turmoil. On the one hand, allowing its currency to decline may help its economy, but if it gets out of hand, China will become significantly destabilized. Thus, I believe the CCP will likely look to sell US assets over the coming year to offset the currency burdens of its immense stimulus policies.

If we consider China’s historically higher interest rate to inflation spread and net exports, it would follow the Yuan should strengthen against the US dollar. In my view, if China were to sell US debt assets, then US long-term rates would likely rise, slowing the US economy already burdened by high rates. Further, that could encourage selling US dollar assets from other countries, potentially shifting their instability to the US.