National Bank of Canada: The Best Of The Big 6 Canadian Banks (TSX:NA:CA)

JHVEPhoto

Please note all $ figures in $CAD, not $USD, unless otherwise stated.

Introduction

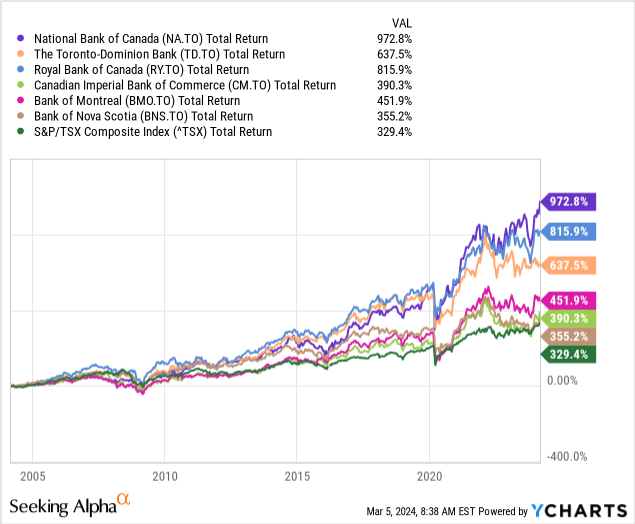

Unlike in the U.S. where the largest companies on the stock exchange are dominated by large technology companies, in Canada, the largest companies are mostly banks. Making up 31% of the TSX, the Big 6 banks have been stellar performers for investors who’ve held on for the long run. In the last 20 years, while the TSX has delivered a total return of 329% (or 7.5% on an annualized basis), the banks have delivered returns considerably higher. In the case of the National Bank of Canada (TSX:NA:CA), the best-performing of the group, the total return to shareholders has been more than a 10-fold increase in the last two decades for an annualized return of 12.6%.

Year by year, the National Bank of Canada has delivered consistent results to shareholders, and its recent quarter for Q1 2024 was no different. As the smallest of the Big 6 banks in Canada with diversified financial services across Canada, the company does everything from personal and consumer loans, mortgages, wealth management services, and insurance. In this article, I’ll delve deeper into the recent results of the company and share my thoughts on its outlook, potential risks, and current valuation.

Recent Results and Outlook

When looking at the recent quarterly results for the National Bank of Canada, the company reported a beat on both revenue and EPS with revenue clocking in at $2.82 billion, up 4.0% year over year (a beat of $113.7 million), and EPS coming in at $2.59, up 2.0% year over year (compared to consensus estimates of $2.35).

At quarter-end, the National Bank of Canada had a ROE of 17.1% and a CET1 ratio of 13.5%. Compared to the rest of the Canadian banks, it had the highest ROE beating EQB Inc. (EQB:CA) at 15.0%, Canadian Imperial Bank of Commerce (CM:CA) at 13.5%, Royal Bank of Canada (RY:CA) at 13.1%, The Bank of Nova Scotia (BNS:CA) at 11.8%, The Toronto-Dominion Bank (TD:CA) at 10.9% and Bank of Montreal (BMO:CA) at 7.2%. As ROE measures how efficiently banks manage their assets and liabilities to earn profits, it would seem that the National Bank of Canada is doing very well in this regard. With a CET1 ratio of 13.5%, the company has very good capital adequacy and has reserves beyond what is required to be considered ‘well-capitalized’.

Looking at the revenues by segment, the National Bank of Canada had revenues up across all of its major segments (except Credigy). In P&C banking, for example, revenues were up 5% driven by strong loan growth. As the company’s largest segment, it was encouraging to see personal and commercial loans up 2% and 11% year over year, respectively. This also translated to pre-tax pre-provision earnings being up 5% as well. Overall, earnings growth in the P&C business is very strong, and the company does have positive operating leverage. While this segment is likely to be more economically sensitive than the other segments, my view is that this segment can grow around 6-7% long-term, consistent with what the company has been able to deliver in the past.

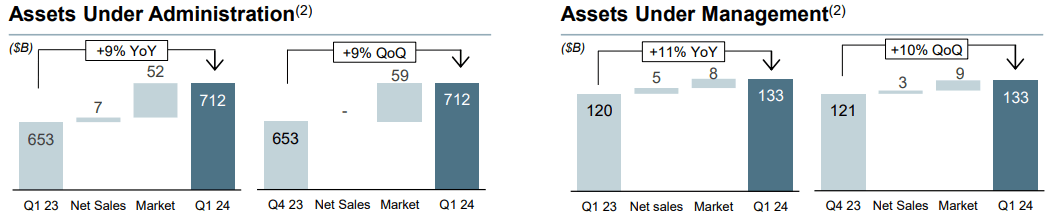

In the Wealth Management business, one of the National Bank of Canada’s faster-growing segments, the company had record quarterly revenues of $660 million, up 4% year over year. This was driven largely by fee-based revenues which were up 8%. Assets under administration climbed 9% and assets under management increased 11%, highlighting market appreciation gains increasing the underlying asset values. For me, the wealth management business is an exciting part of the National Bank of Canada’s business. As Canada nears a $2 trillion market for wealth management, I expect that the National Bank of Canada will be a major beneficiary with its growing wealth management division and I think their faster growth in AUA and AUM indicates that they will likely grow their wealth management division faster than the other Canadian banks.

Investor Presentation

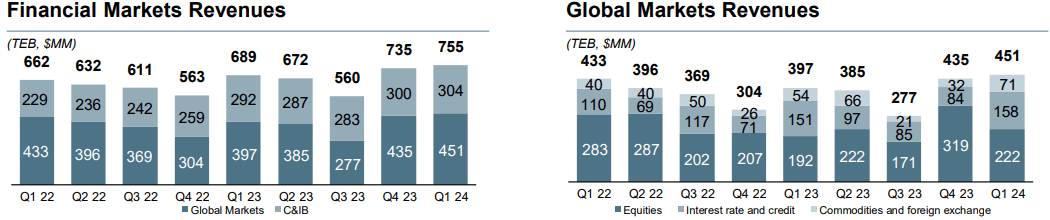

Financial Markets, the segment that deals with all the National Bank of Canada’s corporate and investment banking, advisory, and debt and equity underwriting services, also showed some impressive growth. For the quarter, in Global Markets, quarterly revenues were up 14% year over year and Corporate and Investment Banking was up 4% year over year, led by a steadily improving market for new issuances. In my view, I would continue to expect steady growth in the mid-single digits range for the segment long-term. Why? Despite a relatively softer market for new issuances during the back half of the pandemic, the National Bank of Canada has still managed to put up steady gains year to year for this segment so unless we get some unforeseen headwinds like a recession, we can likely expect fairly modest growth in the Financial Markets segment.

Investor Presentation

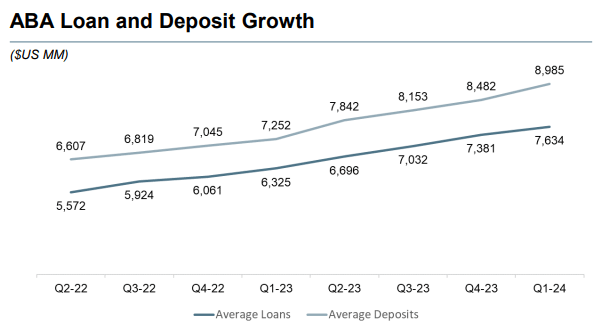

Finally, under the company’s U.S. Specialty Finance and International segment, which includes revenues from both Credigy and ABA Bank, results were strong with 12% asset growth under Credigy and 8% revenue growth for ABA Bank. Credigy has been doing well due to improvement in investment volumes as well as another $1.3 billion invested during Q1. ABA Bank also performed very well with a 28% growth in client base led by continued investments and growth in both loans and deposits. Results have been fairly consistent quarter to quarter, and it seems to me that the accelerated growth rate implies market share gains while maintaining a healthy credit position. About 98% of the loan book is secured with an LTV ratio in the mid-40s, so I would view the loan portfolio as quite healthy and manageable.

Investor Presentation

Risks

Overall, this was another positive quarter for the National Bank of Canada. There’s been a lot of talk lately about a potential recession impacting Canadian banks, but that doesn’t seem to have materialized yet. I won’t pretend to know when a recession will occur, but it seems that even if that was the direction we were heading, I wouldn’t fret too much if I were an investor in the National Bank of Canada.

Secured lending accounts for 95% of retail loans and the bank’s and auto loans make up less than 2.5% of total loans. So even with the recent rise in non-mortgage payments like credit cards and car loans, the National Bank of Canada seems to be a bit more insulated compared to the Big 5 banks.

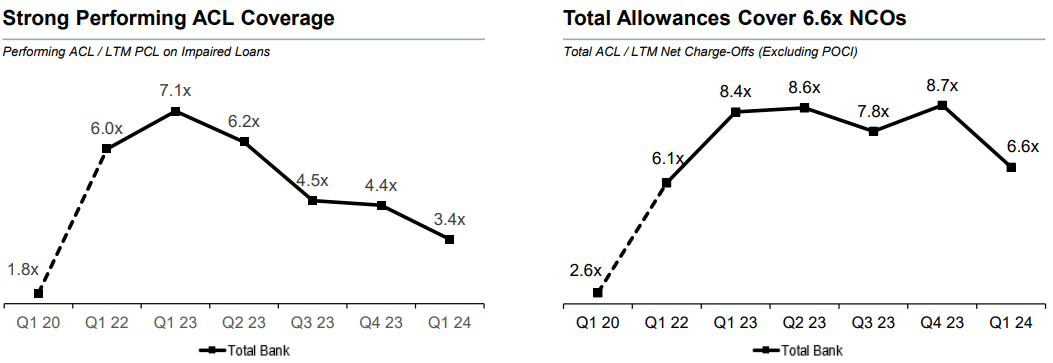

Some investors might be worried about allowance and provision for credit losses and that banks might start to incur big losses ahead in the near future if a recession were to hit the banks. But when we look at the ACL coverage, we can see that the National Bank of Canada has been setting aside more than what would be required to satisfy an estimate for losses. So that makes the allowances look particularly worse today, even before they start to incur losses in their loan books.

Investor Presentation

Even though Canada’s growth was at its slowest pace since 2016, I don’t think it’s appropriate to sound the alarm for a recession without sufficient evidence to support it. Sure, things can get worse from here. But the way the bank is being valued today indicates that much of the risks are likely priced in and that those provisions may prove to be too conservative if, in fact, it turns out to be the case that we don’t head into a recession with mounting impaired loans.

Valuation

Based on the 9 sell-side analysts who cover the National Bank of Canada’s stock, there are 2 ‘buy’ ratings, 6 ‘hold’ ratings, and 1 ‘sell’ rating. The average price target is $109.48, with a high estimate of $112.84 and a low estimate of $107.85 (source: TD Securities). From the current price to the average price target one year out, this implies a potential upside of 2.6%, not including the current dividend of 4.0%. With a total return potential of 6.6%, this implies that analysts are moderately bullish on the near-term upside potential of the National Bank of Canada’s stock.

Overall, I’d say that the National Bank of Canada is probably one of the best-run Canadian banks out there with a superior ROE and a more conservative balance sheet. Looking at the comps table below, the National Bank of Canada’s valuation is right in line with the peer group, so I wouldn’t say that it’s particularly expensive today. With a 4.0% dividend per share, a bit lower than the rest of the peer group, the National Bank of Canada pays out only 43% of its earnings, indicating that it invests more for growth. Hence, I would expect a combination of both capital appreciation and dividend growth in the future from the National Bank of Canada.

Author, based on data from TD Securities and S&P Capital IQ

Conclusion

In summary, the National Bank of Canada reported another strong Q1 which leaves it off to a great start to 2024. Despite some risks related to its international exposure through ABA Bank (Cambodia exposure) and higher credit losses in 2024 compared to last year, the National Bank of Canada’s allowance for credit losses has likely captured most of the losses already. It doesn’t have auto loan exposure or significant mortgage exposure in the more frothy markets in Canada like Vancouver and Toronto. Overall, with strong growth across P&C, wealth management, and financial markets, I think the National Bank of Canada seems to be one of the better ones among the Canadian banks. For these reasons, I rate shares as a ‘buy’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.