SilverCrest Metals: A Value Play In The Silver Sector (NYSE:SILV)

MariuszSzczygiel

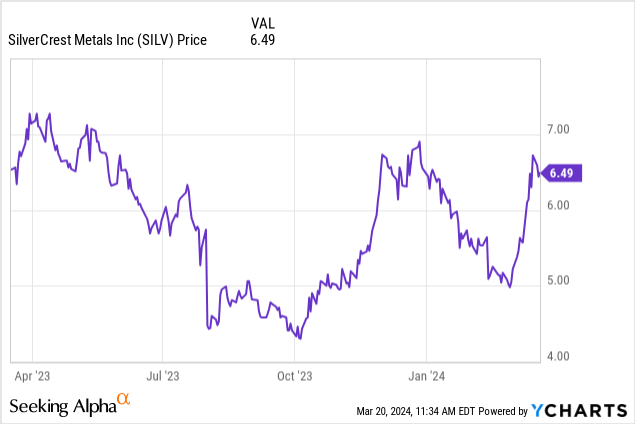

SilverCrest Metals Update

YCharts

This is an update on my previous coverage of SilverCrest Metals Inc. (NYSE:SILV). In November 2023, I called the stock as a Buy due to its robust production numbers and cost efficiency in the third quarter. Since that recommendation, the stock has appreciated nearly 19%, outperforming the S&P 500 (SP500), VanEck Gold Miners ETF (GDX), and Global X Silver Miners ETF (SIL).

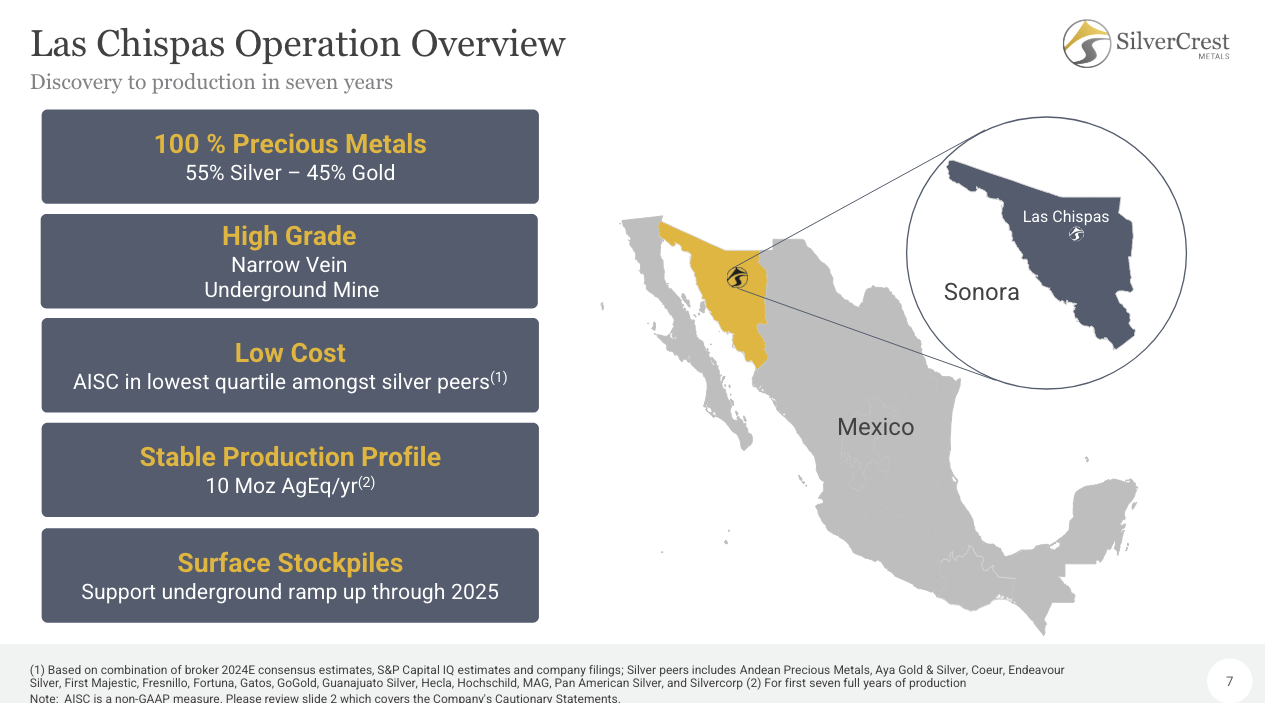

For context, SilverCrest operates the Las Chispas Mine in Sonora, Mexico, located about 180 kilometers northeast of Hermosillo. The mine is projected to operate for eight years, producing 57,000 ounces of gold and 5.5 million ounces of silver annually, which equates to 10 million silver equivalent ounces, all at the low all-in cost of $11.98 per silver equivalent ounce.

With gold and silver prices at $1,800 and $23.00 per ounce, respectively, the mine’s net present value, after taxes and at a 5% discount rate, is estimated at $549.9 million. The company also plans to further explore the mine’s potential through a $10 million program targeting a significant portion of its inferred mineral resources.

As an operational mine, Las Chispas has been performing remarkably well. For 2024, SilverCrest projects production between 9.8 and 10.2 million silver equivalent ounces, with all-in sustaining costs (AISC) between $15.00 and $15.90 per ounce, closely aligning with the technical report’s forecast of $15.08 AISC per ounce. And, in the last quarter, the company reported a net free cash flow of $33.4 million, or $0.23 per share.

With SilverCrest’s stock climbing even higher following an impressive Q4 earnings report, the question remains: are its shares still a good value and worth buying? Let’s delve into the analysis below.

SilverCrest: What Happened in Q4?

SilverCrest Metals

SilverCrest Metals reached its year-to-date highs this week, spurred by an earnings report that surpassed expectations with increased sales and rising metal prices.

The company’s Q4 performance was exceptional. The quarter saw a robust 41% increase in gold sales to 16.1 thousand ounces, up from 11.4 thousand ounces in the prior year’s quarter, while silver sales rose by 35% to 2.56 million ounces from 1.89 million ounces.

It reported net earnings of $35.9 million, or $0.24 per share, a significant jump from $5.2 million, or $0.04 per share, in the same quarter last year-during which the miner was only in its second month of commercial production.

This not only represented a substantial increase over the third quarter’s earnings, but also exceeded the $0.11 per share consensus estimate from analysts. Revenue also saw a notable increase, up 50% year-over-year to $61.3 million, beating the analyst consensus of $59.5 million.

Readers should also note that SilverCrest reported an average realized price of $1,979/oz Au and $23.09/oz Ag in Q4, and spot prices are now well above these levels.

Looking ahead, SilverCrest anticipates the Las Chispas underground operation in Mexico to continue its ramp-up throughout 2024. Mining rates are expected to stay consistent with Q4 levels during the year’s first half before increasing in the second half, aiming for an exit rate of 1,050 metric tons daily.

SilverCrest Metals

For 2024, SilverCrest projects production sales volumes to be between 9.8 million and 10.2 million gold equivalent ounces, with all-in-sustaining costs estimated to be between $15.00 and $15.90 per gold equivalent ounce sold.

Another significant achievement for SilverCrest was becoming debt-free within just seven months after beginning commercial production, having paid off $50 million in debt.

SilverCrest Metals

Beyond repaying debt, the company invested $37.2 million in 2023 towards share repurchases, exploration activities, and increasing its bullion reserves, concluding the year with a robust treasury and $175 million in total liquidity.

Although the company expects a slower increase in cash reserves in 2024 due to upcoming tax obligations and costs related to contractor services, SilverCrest is poised to continue its strong cash flow generation this year.

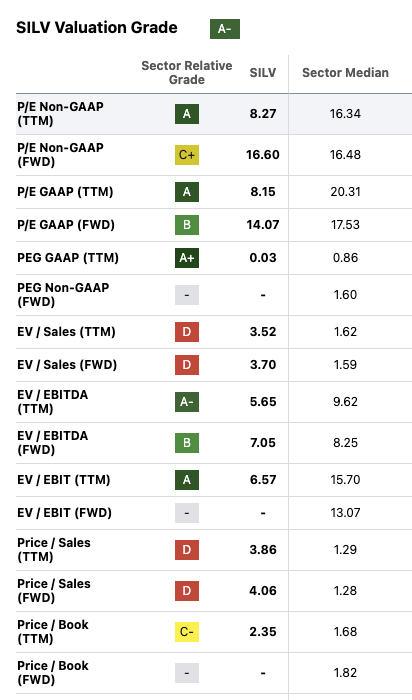

SilverCrest’s Valuation

Seeking Alpha

SilverCrest’s valuation has become even more enticing following its robust fourth-quarter earnings.

The company reported earnings per share (EPS) of $0.24 in Q4. Although its price-to-earnings (P/E) ratio stands at approximately 8 according to Seeking Alpha, my analysis suggests a much more compelling forward P/E of 7x when considering full-year EPS projections close to $1, based on current precious metal prices. This places SilverCrest significantly below the industry median P/E of 17x, offering a substantial discount for investors.

Adding to its appeal, SilverCrest is now debt-free and boasts a strong net cash position. The company can expand the Las Chispas mine and support its share buyback initiatives, reinforcing the case for investing in its stock.

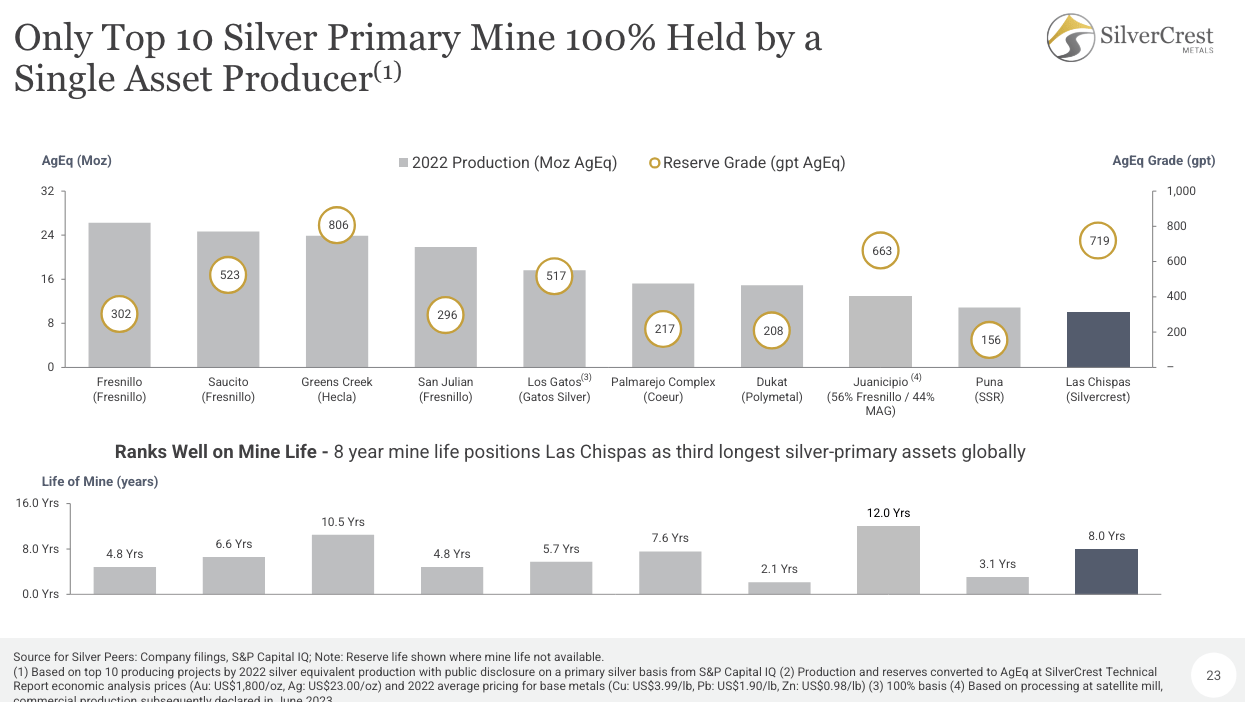

SilverCrest: M&A Candidate

SilverCrest Metals

The sweetener to SilverCrest’s investment thesis is its attractiveness as an acquisition target.

SilverCrest uniquely owns 100% of one of the top 10 primary silver mines within a favorable jurisdiction, positioning it as a prime candidate for acquisition by larger industry players.

I believe the mine’s low operational costs, notable profitability, and a lifespan extending beyond eight years enhance its appeal to companies such as Hecla Mining Company (HL), Coeur Mining, Inc. (CDE), Pan American Silver Corp. (PAAS), and SSR Mining Inc. (SSRM), which may see strategic value in acquiring SilverCrest in the foreseeable future.

SilverCrest: The Bottom Line

SilverCrest Metals has demonstrated strong performance since my BUY recommendation in November 2023, capitalizing on robust production and cost efficiency at its Las Chispas Mine. With its shares appreciating nearly 19% since then, SilverCrest has not only outperformed major indexes but also shown significant growth in a vibrant precious metals market.

Despite recent achievements, including an impressive Q4 earnings report that surpassed analyst expectations, the question arises: does SilverCrest still present a valuable investment opportunity?

With a forward P/E ratio suggesting a deep discount compared to industry standards, debt-free status, and substantial cash reserves, SilverCrest appears well-positioned for future growth and potential acquisition interest from industry giants.

Considering these factors, SilverCrest remains a compelling buy for investors looking to capitalize on the ongoing silver price rally.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.