Foot Locker Q4 Earnings: Promotions Drive Topline Beat, Shares Fairly Valued (NYSE:FL)

Justin Sullivan/Getty Images News

Shares in Foot Locker (NYSE:FL) have been on a tear over the last six months. Prior to the release of its Q4 earnings this morning, shares were up nearly 80% during this time span. Based on the immediate market reaction following today’s release, investors had reason to sell into results despite FL’s beat on both the top and bottom lines.

Seeking Alpha – 6M Share Price Performance Of FL

In my last quarterly update on FL following Q3 results, I noted that shares were fairly valued for the macroeconomic environment, one that consisted of a still-cautious consumer with a preference for value ahead of the holiday season. I also noted that the promotional period for FL may stick around for longer than desired due to elevated inventory balances.

Shares gained 22.5% since that update, more than double that of the broader S&P 500 (SPY) in the same period. While the gains slightly trail that of Hibbett, Inc. (HIBB), which is up nearly 30%, shares in FL have significantly outperformed NKE since FL’s Q3 results.

Seeking Alpha – Share Price Performance Of FL Relative To Peers Since Last Author Update

Following Q4 results, which topped expectations at both the top and bottom lines, I remain neutral on shares of Foot Locker due to continuing topline weakness and the current lack of data surrounding newly announced strategic initiatives. Here’s what else investors should know about FL’s Q4 results.

What Did Foot Locker Expect Heading Into Q4 Results?

As part of full-year and quarterly guidance provided in the Q3 commentary, CFO Mike Baughn updated investors with a narrowed outlook.

Full-year non-GAAP EPS was set to a range of $1.30/share to $1.40/share, down $0.10/share at the top of the range. The corresponding sales outlook inclusive of an extra week, on the other hand, was favorably revised to a range of down 8% to 8.5% from 8% to 9% previously.

Specific to Q4, the management team expected non-GAAP EPS to land in a range of $0.26/share to $0.36/share or $0.31/share at the midpoint. The range was based on the view that comparable sales would be down 7% to 9%, reflecting a cautious holiday consumer at the low end of the range.

Gross margins were also expected to track in a range of 27% to 27.2%, representing a YOY decline of 290 basis points and 310 basis points, respectively. At an operating level, rising SG&A costs were expected to deleverage by 40 to 70 basis points, with SG&A as a percentage of sales expected to fall between 22.7% and 23%.

Recap Of Foot Locker’s Q4 Results

Early momentum in the holiday season noted in Foot Locker’s earlier Q3 earnings commentary appeared to extend for the entirety of the quarter. Though the company still reported a comparable sales decline of 0.7% during the quarter, the decline was significantly better than the 7% to 9% decrease that was initially expected.

CEO Mary Dillon noted the sales were driven by a combination of full-price selling and “compelling promotions.” The promotional activity, however, was likely greater than most had expected. Heading into the quarter, FL expected gross margins to be down YOY by 290 to 310 basis points. Instead, margins were down 350 basis points due in part to the higher markdown activity.

Despite the lower gross margin, FL realized bottom line leverage through the better than expected topline result. This contributed to overall non-GAAP EPS in Q4 of $0.38/share or $0.02/share above the topline of the guidance range.

What Is The Sales And Earnings Outlook For Foot Locker?

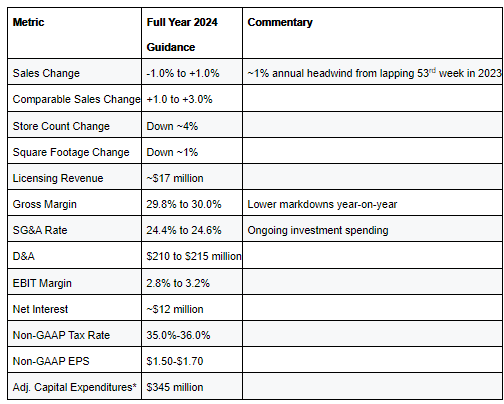

Looking ahead to fiscal 2024, FL expects the overall sales trend to be essentially flat, in a range of down 1% to up 1%. Sales on a comparable basis, on the other hand, are expected to be 2% at the midpoint of the range.

In the new year, FL also expects to expand bottom line profitability, with EBIT margins expected to land in a range of 2.8% to 3.2%. This factors in the ongoing deleverage from continuing investment spending on strategic initiatives, with SG&A as percentage of sales expected at 24.4% to 24.6% of sales.

FL Q4 Earnings Release – Summary Of Fiscal 2024 Guidance

Despite the better outlook for EBIT in fiscal 2024, CFO Mike Baughn noted that there would be a two-year delay in achieving their long-term EBIT margin target of between 8.5% to 9%. This target is now expected to be reached in 2028.

Additionally, FL sees fiscal 2024 as a cash rebuilding year. As such, the company noted that the dividend would not return at this point in time.

Is FL Stock A Buy, Sell, Or Hold Following Q4 Results?

Shares in FL have rebounded quite nicely after hitting their mid-teens 52-week low earlier in the year. Bullish sentiment in recent periods could be attributable in part to positive analyst upgrades. In the last three months, there have been four and six upward revisions in annual EPS and revenue targets, respectively.

Analysts are especially optimistic about FL’s ability to drive margins in the periods ahead. In December, Piper Sandler upgraded the stock to “overweight” due in part to healthier inventory levels, which factor into the extent of FL’s promotional activity as well as to FL’s capacity to introduce newer product offerings.

FL has also been the subject of speculation surrounding an activist investor. Earlier in February, a report from Insightia’s Activist Insight noted that the retailer’s overall share price performance over the last year made it vulnerable to external interest. In my view, this is unlikely. FL appears to be making strides in ongoing turnaround efforts. Recently announced initiatives, such as its entrant into India, may also instill optimism in greater topline growth.

Despite its bullish turn, most remain neutral on Foot Locker’s prospects. The stock grades poorly on Seeking Alpha’s quant metrics due to its current valuation and its weak growth and profitability outlook. Wall Street is similarly neutral. In fact, one could even say that Wall Street is pessimistic. For example, while FL may have earned an upgrade from Piper, the consensus Wall Street price target stands at about $26/share. This would represent over 20% downside risk in the shares.

In my view, the announcement of new strategic initiatives in 2023, including a new multi-year partnership with the NBA, as well as the pending fiscal 2024 entry into India, are positive developments that could support topline growth in the periods ahead. However, there is uncertainty whether these initiatives will bear fruit.

The company is also facing challenges relating to sales growth. While comparable sales came in much better than expected in Q4, much of the momentum appears to have been driven by promotional activity. The stock has turned in worthy gains for investors who have held on through the good and the bad. In my view, investors would be best suited to remain on hold until further progress is reported at the topline and in FL’s ongoing strategic initiatives.