First Majestic Silver: A Slow Start To The Year (NYSE:AG)

Evgeny Gromov

The Q1 Earnings Season for the precious metals sector is just around the corner and one of the more recent names to release its Q1 production numbers is First Majestic Silver Corp. (NYSE:AG). Unfortunately, the company had a tough quarter because of lapping difficult year-over-year comps, reporting silver and gold production down 22% and 41%, respectively. However, it’s important to note that a large chunk of the decline in gold production was related to it placing Jerritt Canyon in care & maintenance, and both San Dimas and La Encantada should have a better H2 with higher grades and higher throughput, respectively.

In this update, we’ll dig into the Q1 production figures, its FY2023 reserve update, and where the stock’s updated buy zone lies:

Jerritt Canyon Site – Company Website

All figures are in United States Dollars unless otherwise noted.

Q1 Production

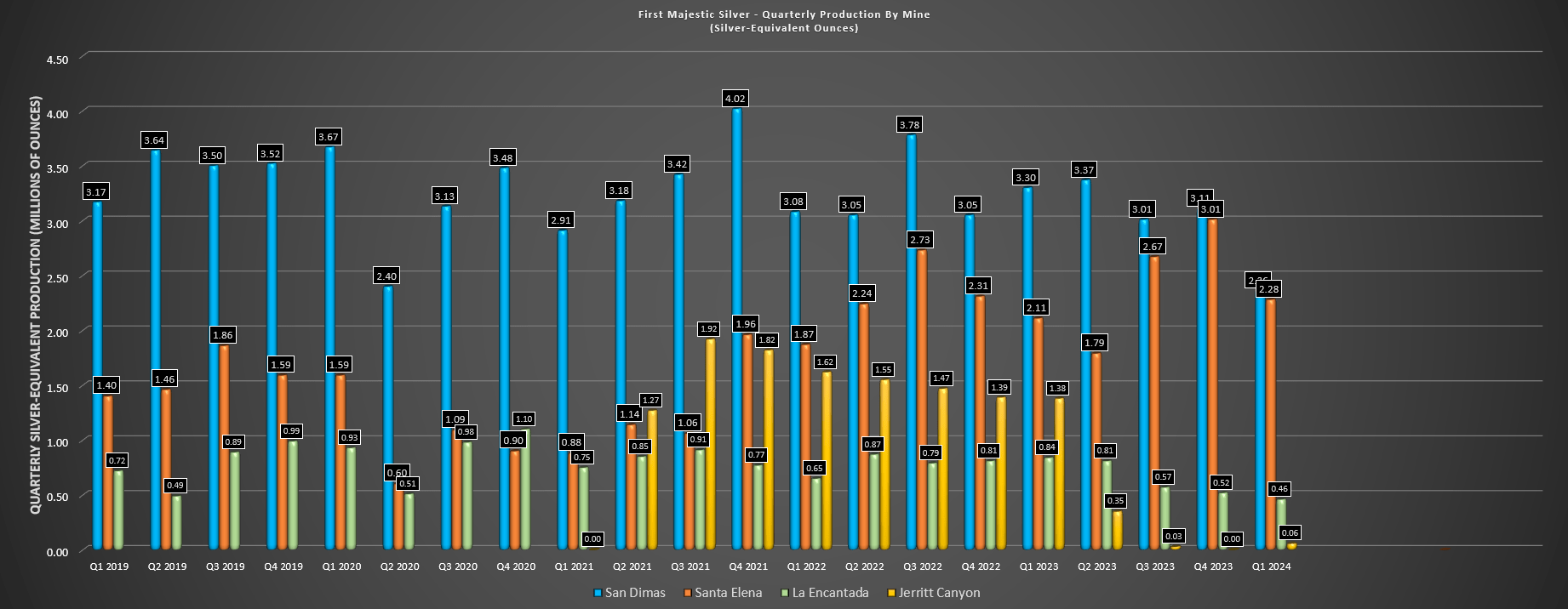

First Majestic Silver (“First Majestic”) released its preliminary Q1 results last week, reporting quarterly production of ~1.98 million ounces of silver and ~35,900 ounces of gold. This translated to high double-digit percentage declines in production from the year-ago period and ~5.2 million silver-equivalent ounces [SEOs], with the largest decline being in gold production (down 41% year-over-year). However, as noted previously, its Jerritt Canyon Mine was the main culprit for the decline in gold production, with production sliding from ~16,300 ounces to ~600 ounces as the asset was moved into care & maintenance in Q2 of last year.

First Majestic Silver – Quarterly SEO Production by Mine – Company Filings, Author’s Chart

Moving over to silver production, San Dimas produced just ~1.16 million ounces of silver and ~13,500 ounces of gold, both sharp declines from the year-ago period. This was related to lower throughput and grades of ~178,000 tonnes at 220 grams per tonne of silver and 2.45 grams per tonne of gold (Q1 2023: ~219,000 tonnes at 241 grams per tonne of silver and 2.98 grams per tonne of gold). However, grades were well below reserve grades in Q1 2024 (260 G/T silver/3.11 grams per tonne of gold) and are expected to tick up as the year progresses with mining during Q1 in lower grades areas of the Central and Graben blocks. Hence, we should better margins and revenue from this asset in H2 2024.

Meanwhile, La Encantada saw significantly lower production of ~456,000 ounces of silver (Q1 2023: ~836,000 ounces) due to water availability issues which appear to be in the process of being resolved. This is because hole G11 has identified “a significant water source” according to First Majestic, which should result in processing rates moving back towards 3,000 tonnes per day in Q3 and improving on a sequential basis. Hence, with two of its three silver operations seeing much weaker Q1 performances, it’s no surprise that we saw a material decrease in silver production year-over-year.

Fortunately, First Majestic’s Ermitano Mine had a solid quarter, processing ~224,400 tonnes at 72 grams per tonne of silver and 3.16 grams per tonne of gold at significantly higher recovery rates of 69% and 95% for gold and silver, respectively. This translated to Q1 production of ~355,000 ounces of silver and ~21,700 ounces of gold vs. ~104,000 ounces of silver and ~24,000 ounces of gold in the year-ago period. So, while the company had a tougher quarter from its two other silver mines, Ermitano continues to fire on all cylinders and was able to pick up some of the slack (with a further benefit from record gold prices) to offset what would otherwise have been a significant revenue decline for the company year-over-year.

Updated Reserve Base

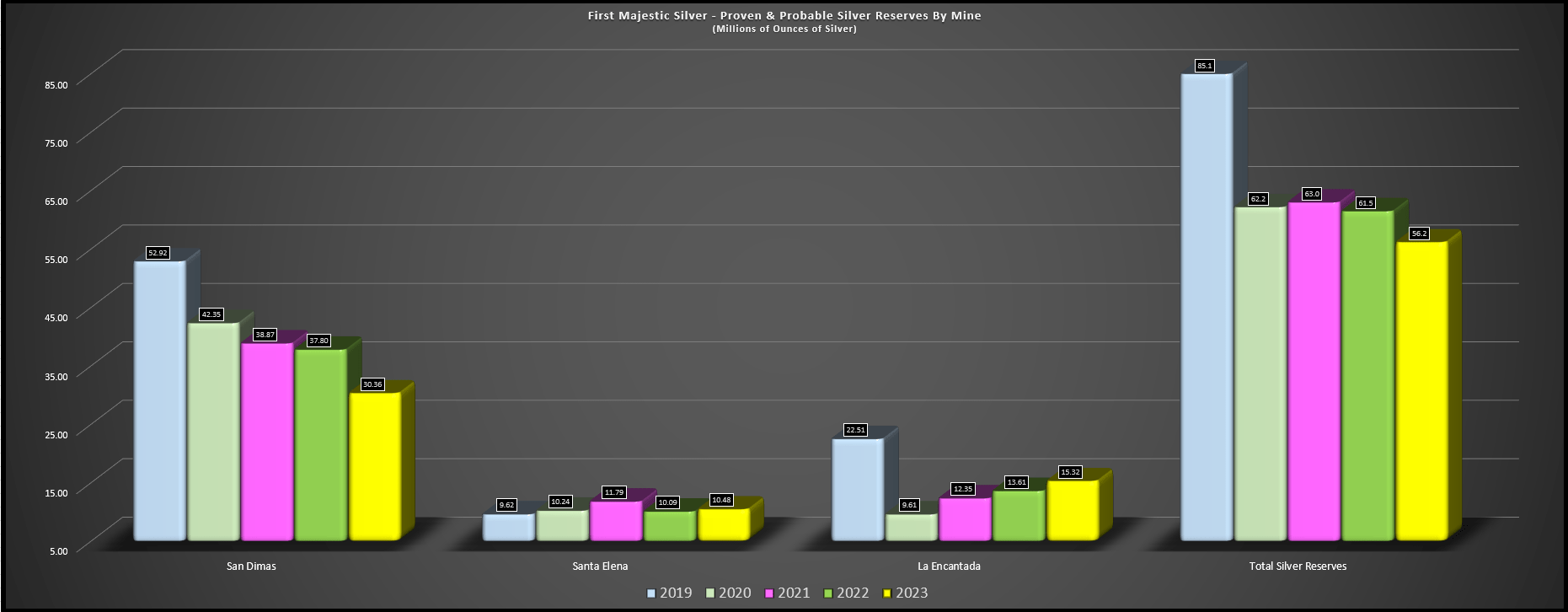

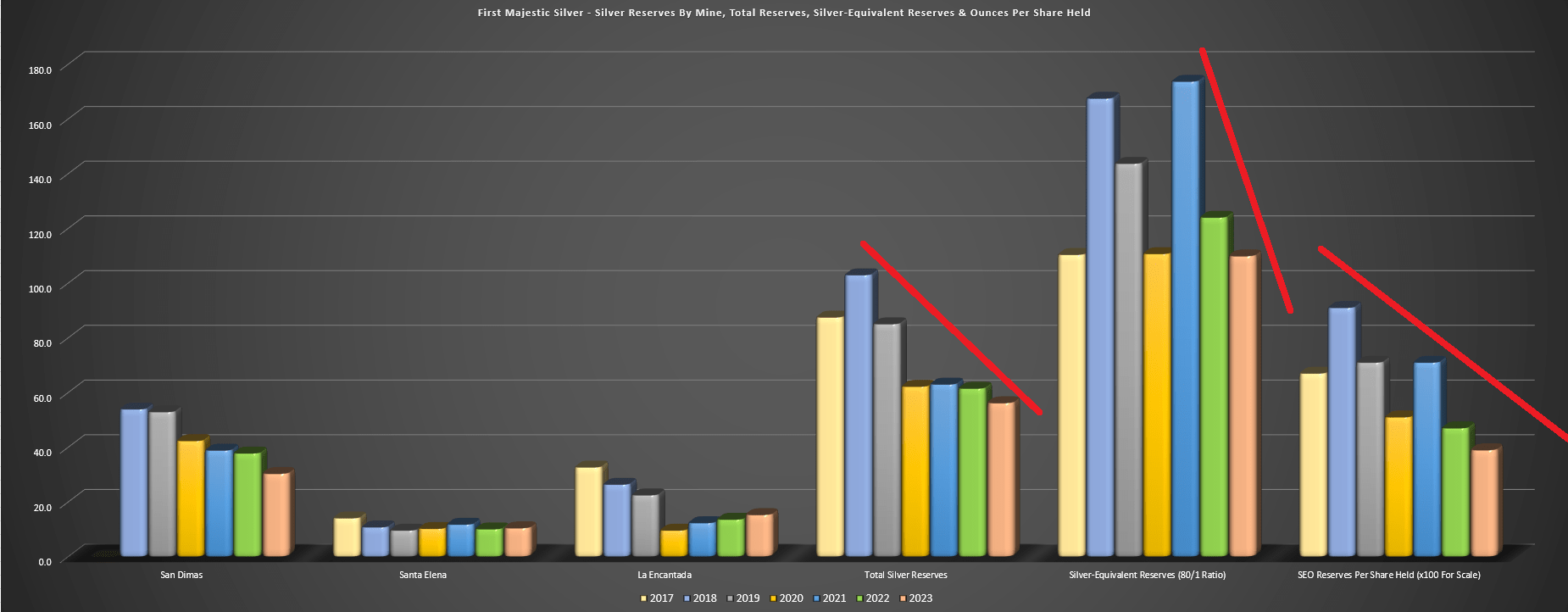

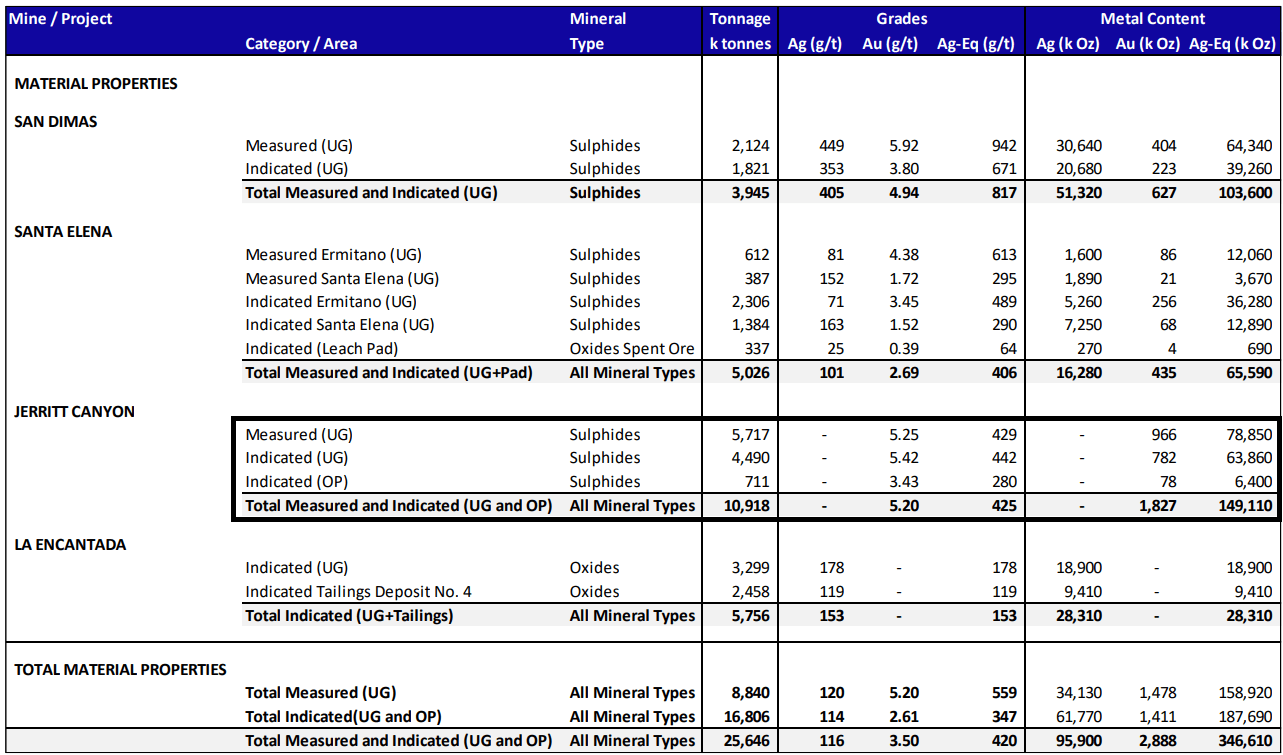

As for First Majestic’s year-end 2023 reserve base, we saw a significant decline in silver reserves to ~56.2 million ounces, which marked the second consecutive annual decline in a row. The sharp decline in silver reserves was driven by lower reserves at the company’s San Dimas Mine, which is also subject to a significant gold stream held by Wheaton Precious Metals (WPM), with silver reserves declining from ~37.8 million ounces to ~30.4 million ounces, and declining for the fifth consecutive year. This was partially offset by a slight increase in reserves at Santa Elena and an increase in reserves at La Encantada, which finished the year with ~10.5 and ~15.3 million ounces of silver, respectively. The lower reserves at San Dimas were related to a higher cut-off grade and the exclusion of low tonnage pillars, with reserve tonnes down from ~4.3 million tonnes to ~3.6 million tonnes at lower grades (521 grams per tonne silver-equivalent vs. 550 grams per tonne silver-equivalent).

First Majestic Silver Annual Silver Reserves – Company Filings, Author’s Chart

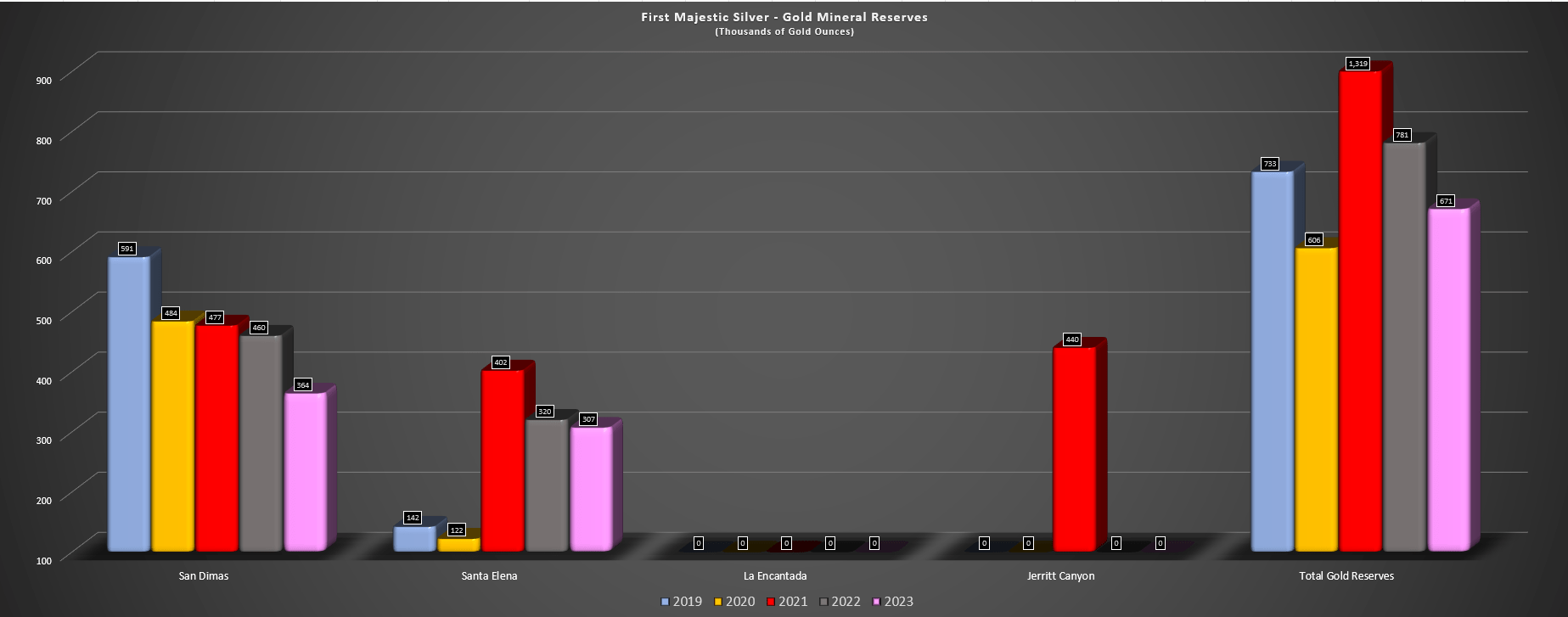

As for gold reserves, we saw a decline in the reserve base here as well, with lower gold ounces at both San Dimas and Santa Elena. As for Santa Elena, gold ounces at its currently producing Ermitano Mine declined from ~274,000 ounces to ~266,000 ounces, while we saw a marginal decline in ounces at Santa Elena. The result is that First Majestic’s silver-equivalent ounce [SEO] reserve base fell to just ~110 million ounces, a more than 10% decline from the year-ago period. And as the chart below highlights, this resulted in a further decline in SEO reserves per share when combined with share dilution from ATM sales, which is not what investors want to see.

First Majestic Silver Gold Mineral Reserves (000’s of Gold Ounces) – Company Filings, Author’s Chart First Majestic Silver Reserves by Mine, Total Reserves, Silver-Equivalent Reserves & SEOs Per Share Held – Company Filings, Author’s Chart

To better explain the latter point, investors in this industry should not focus on companies that are growing, but companies that are growing on a per share basis. This is because growth without per share growth is not meaningful as it means that shareholders are ultimately not seeing the benefits of that growth in either production, cash flow, and or resources/reserves per share. And if one is investing in the precious metals sector, they are better off owning the metal themselves (gold/silver) than a company with consistently declining per share metrics and a (*) relatively small reserve base. (*)

(*) First Majestic’s reserve base sits at just ~10.0 million tonnes based on San Dimas, Ermitano and La Encantada, translating to a sub 4-year mine life for its silver operations assuming an average processing rate of ~2.7 million tonnes per annum. (*)

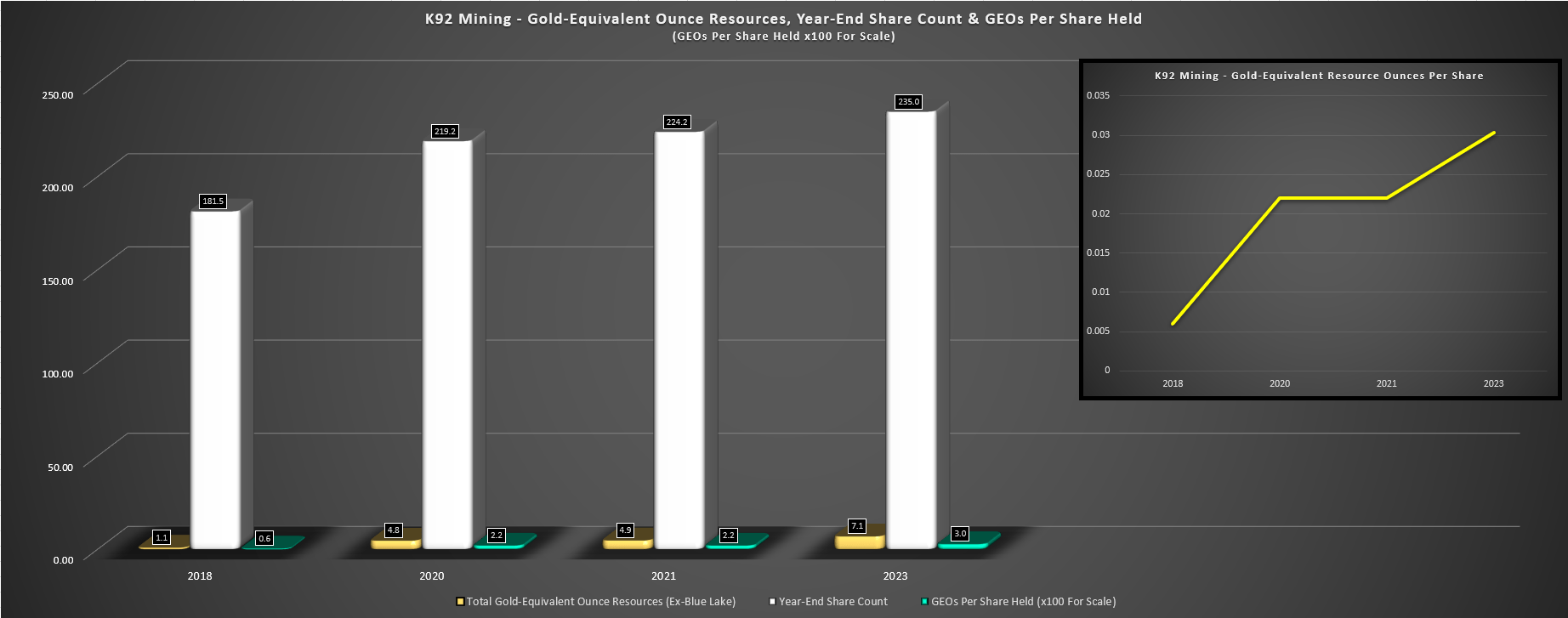

For investors looking for companies with industry-leading growth that’s also translating to significant per share growth, K92 Mining is a far more superior option, with an industry-leading growth profile shown below. In fact, in the same period that First Majestic’s SEOs per share has declined by over 50% (2018 to current), K92 Mining’s gold-equivalent ounces per share have grown over 5x and will continue to grow with their new Arakompa regional opportunity. Meanwhile, K92 Mining is in the process of transforming from a ~130,000 ounce per annum producer with average costs to a ~470,000 ounce per annum producer with sub $700/oz AISC which will give it the highest-grade, highest-margin and largest producing asset not held by a major in 2027.

K92 Mining Gold-Equivalent Ounce Resources & GEOs Per Share Held – Company Filings, Author’s Chart

Recent Developments

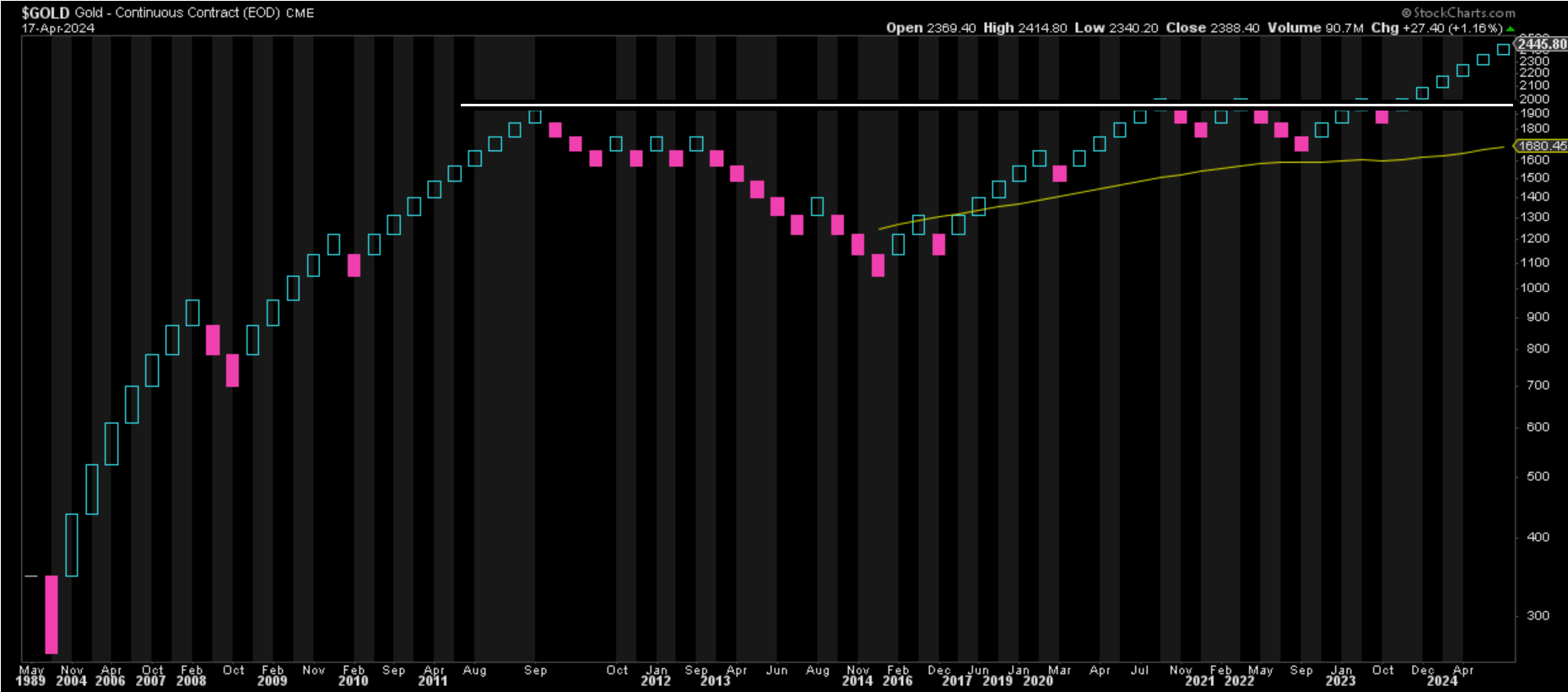

While the silver price appears to have broken out above lower resistance in the $26.60/oz area, First Majestic is also benefiting from a much higher gold price, which has already broken out to new all-time highs. And while some investors may not think this is a significant development for the company, it’s actually quite positive given that its Ermitano Mine produces a significant amount of gold vs. Santa Elena and First Majestic has a large gold project in care & maintenance in Nevada. Obviously, there is no guarantee that Jerritt Canyon can be restarted successfully, but its future is looking much better in a $2,200/oz to $2,400/oz gold price environment than it was at $1,700/oz to $2,000/oz which made it difficult to justify mining at this mid-grade double refractory orebody.

Gold Long-Term Chart – StockCharts.com

As for recent commentary on Jerritt Canyon, First Majestic’s CEO Keith Neumeyer has called the asset “strategic” and this is certainly a fair point. This is because the site owns one of three roasters in the state with over $1.0 billion in sunk costs and the future of mining in Nevada is mostly harder to reach refractory ore vs. a significant portion of mining being the “low-hanging” oxide ore previously. Hence, having a processing facility capable of processing refractory is a significant competitive advantage both from a new discovery standpoint (facility is already there) and a toll-milling standpoint as Barrick (GOLD) and Newmont (NEM) would prefer to feed their own ore to their processing facilities given that Nevada is an important production hub for both companies in their 61.5%/38.5% joint-venture (Nevada Gold Mines LLC).

It’s an important asset, it’s very strategic. It’s one of only three roasters in all of Nevada. We’re being approached by a number of mining companies to use that roaster. A lot of the ore in this region is double-refractory ore, and it needs a roaster to process it – so that roaster is very strategic. We need to drill and we are. Our geologists have some views that there’s an elephant out there somewhere. It’s a big land package, hasn’t really been drilled much – we’re spending $10 million on exploration this year, the largest drill program in probably fifteen years at Jerritt Canyon.

– Keith Neumeyer, First Majestic Silver CEO, Recent BNN Interview

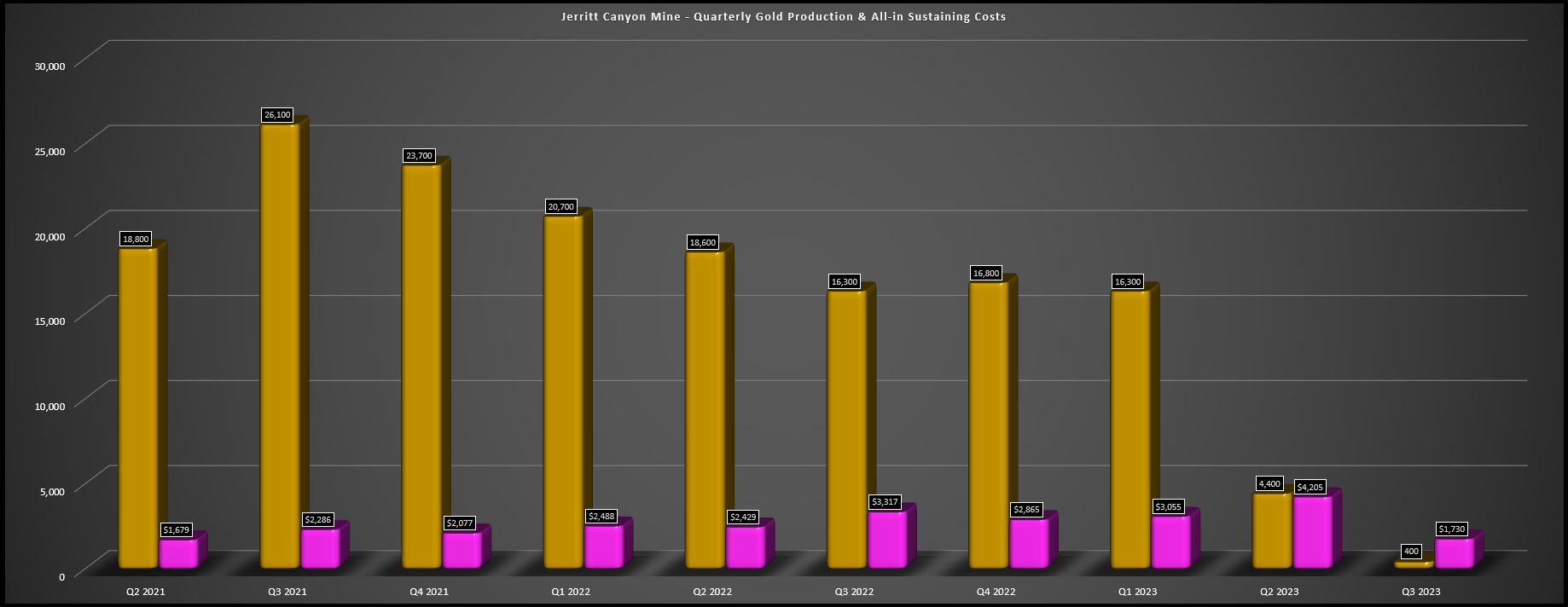

Looking at Jerritt Canyon’s production and cost profile below, the average Q2 2021 to Q4 2022 may not inspire much confidence in restarting this asset (~$2,400/oz AISC) even at current gold price, but it’s important to note that some of this cost profile was related to significant sustaining capital spend, and the asset was running at nowhere near its full capacity. In addition, the company may look to bring its own workforce even vs. a contractor to reduce costs if it were to restart the asset. Hence, if the company can find a way to improve productivity and increase throughput to 3,500 to 4,000 tons per day to leverage the site’s high fixed costs, this could be a very different asset with sub $1,850/oz AISC which would certainly work in a $2,400/oz – $2,500/oz gold price environment.

Jerritt Canyon Quarterly Gold Production & AISC – Company Filings, Author’s Chart

As it stands, Jerritt Canyon has ~1.83 million ounces of gold in the measured & indicated category at 5.20 grams G/T of gold, which is below the ideal grade for a double-refractory orebody with much higher processing costs than an oxide operation. In comparison, Barrick is working to delineate a large-scale 11-13 gram per ton gold discovery at Fourmile which easily justifies trucking this refractory ore from Cortez to process at its shared Carlin Complex. That said, while Jerritt Canyon’s rock value per ton was ~$240/ton post-recoveries at $1,900/oz, this has improved to ~$295/ton at $2,350/oz gold, a significant improvement ($55/ton) that offsets most of its expected processing/G&A costs of ~$70/ton.

It’s important to note that I don’t see a Jerritt Canyon restart as likely in the next 12-18 months, I am cautiously optimistic that this asset might actually pan out for First Majestic if the new reality is a $2,200/oz to $2,600/oz gold price longer-term which turns this into a mid-scale and low-margin operation vs. a site that’s currently collecting dust while First Majestic explores for new ounces. In summary, while Jerritt Canyon was more of a liability than an asset at sub $2,000/oz gold with it turned off given its reclamation and closure costs, this could be restarted at a higher gold price and can be thought of as an optionality play and potentially be a ~160,000 to 180,000 ounce per annum operation with mediocre margins post-2026.

Jerritt Canyon Resources – Company Website

Valuation

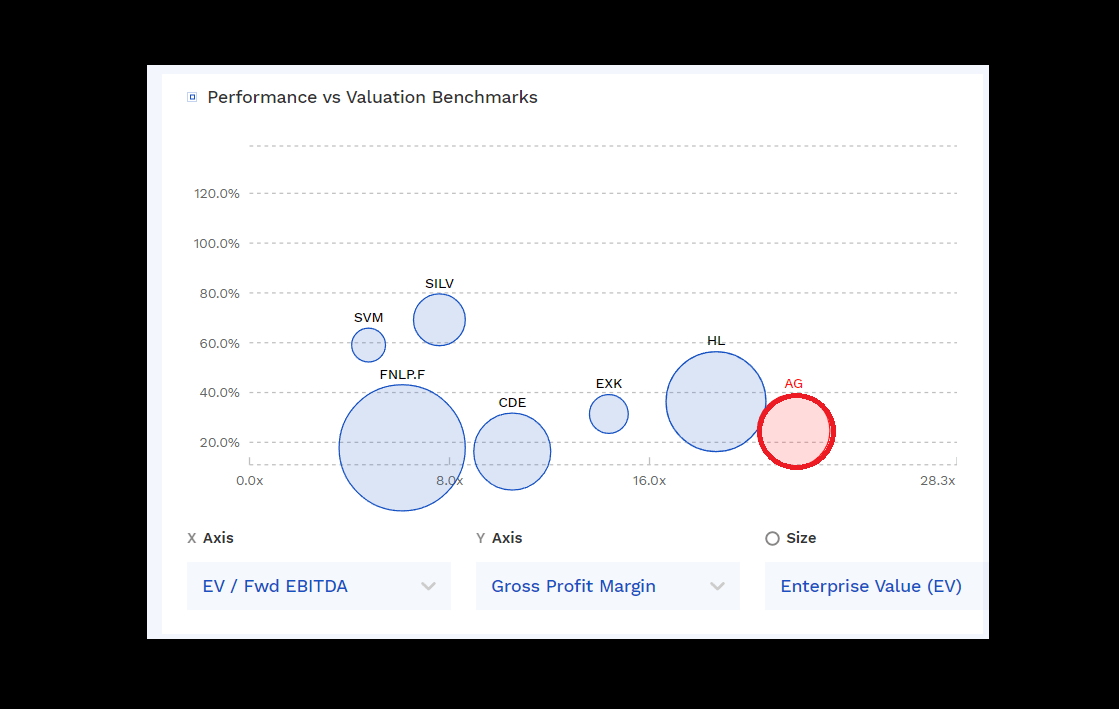

Based on ~290 million fully diluted shares and a share price of US$6.90, First Majestic trades at a market cap of ~$2.0 billion and an enterprise value of ~$2.13 billion. This makes it one of the higher capitalization names in the silver space and also one of the most expensive, trading at nearly 3.0x P/NAV based on an estimated net asset value of ~$650 million and ~$18 per ounce of silver-equivalent reserves even though it’s pulling these ounces out of the ground at cost closer to ~$20.00/oz. Finally, even with the improved metals price environment that should allow it to generate positive free cash flow in 2024 and 2025, the stock is trading at ~40x two-year forward (FY2025) free cash flow estimates even using silver prices just shy of spot levels ($27.00/oz).

To put this valuation in perspective, major producers like B2Gold (BTG) trade at just ~5.4x FY2025 free cash flow estimates, and Endeavour Mining (OTCQX:EDVMF) currently sits at less than 5x FY2025 free cash flow estimates, with both producers sporting industry-leading margins and strong track records of per share growth. As for non-African producers, even Tier-1 jurisdiction producers with stronger organic growth profiles like Alamos Gold (AGI) are trading less than 15x free cash flow or roughly one-third the free cash flow multiple of First Majestic Silver. Hence, with First Majestic being a Mexico-only story with industry-lagging margins that’s struggled to grow per share metrics, I continue to see it as a less attractive name from a relative value standpoint.

First Majestic Silver Valuation & Margins vs. Silver Producer Peers – Finbox

So, what are the positives?

While share sales under its At-The-Market Equity program were a significant drag on the share price in 2022 and 2023 as was significant capex at Jerritt Canyon, the company has a lighter capex profile this year and next and should see average capex closer to ~$100 million. And when combined with positive free cash flow in 2024 and 2025, this should take some pressure off the share price as First Majestic won’t need to be selling any meaningful amount of shares to improve its balance sheet. In summary, while I do not see an attractive valuation setup here for First Majestic, it’s certainly possible that the stock’s rally could continue given that its cash flow outlook has improved materially, we shouldn’t see any meaningful share dilution, and First Majestic remains a go-to name in the silver space given its superior trading liquidity.

ATM Program Proceeds 2022/2023 – Company Filings

Summary

First Majestic Silver had a tough start to 2024 with double-digit declines in silver and gold production. However, this was largely because of lapping difficult comparisons with its Jerritt Canyon Mine since moved into care & maintenance and its La Encantada Mine struggling with water availability issues vs. a full quarter of production in Q1 2023. On a positive note, the company has recently identified a significant water source, which will increase production in H2 from this primary silver mine and while little value has been assigned to Jerritt Canyon, a bull market in gold could be a life rate for this higher-cost asset. Finally, its Mexican production profile may not offer diversification (100% of revenue from Mexico), but they are generating free cash flow at current metals prices.

That being said, I prefer to invest at a significant discount to fair value or pass entirely. And while AG is a name of choice for those looking for a highly liquid silver producer with a significant portion of revenue coming from silver, I continue to see more attractive bets elsewhere in the precious metals sector. So, while I would consider First Majestic from purely a trading standpoint if we were to see a pullback below US$5.50 which would move the stock back into a technical buy zone, I remain focused elsewhere for the time being.